Jump in digital adoption & accelerated UX focused transformation in banking

A Snapshot from Hungary on the effects of Covid19

by István Sebestyén

In a very pleasant climate, after 6 months or so, the other day I met two former colleagues in a terraced brewery next to a trendy shopping center in the inner city of Budapest. All night, we were the only guests on that trendy place. There was the existential uncertainty mixed with the fear of the second wave of Covid19 in the air. This came to my mind as a reflection of the very informative Webinar of Covid19 by Deloitte Digital and Salesforce Hungary in June 2020 with Tamás Schenk, Dániel Drácz, Géza Mátrai, Laura Goci & Zoltán Szőllősi. It induced further thoughts concerning the banking sector.

Changing consumer attitude

In the first wave of Covid19 the sectors critically affected: tourism, aviation, transportation were practically shut down. Exports crashed and there were significant supply chain issues. I think the use of forced leave, reduction of working hours by employers as a first reaction happened on a much wider scale than the 2020 May Deloitte Digital survey indicates. According to which 30% of people suffered from a sizeable income loss with 10% have lost their jobs. The Covid19 crisis due to inequalities in job opportunities and applicability of home office reinforced the already remarkable regional differences among Budapest, Western and Eastern Hungary.

Covid19 effects induced an immediate change in customers’ consumption habits and preferences. 50% of customers have reduced spending. The conscious middle class that has slipped down financially in recent decades has immediately put the strongest brake on shopping. With nearly half of the population’s net financial position is deteriorating, overall savings are growing for precautionary reasons. 21% of surveyed intend to make more savings. 18% is focusing on healthy nutrition and sports because they had freed up time during lock-down. However, it did not convert to a financial product yet, only in case of 1–3%. The increase in consumption in one segment is remarkable, but non-organic, covers one-off expenditures due to the epidemic in my view, to bear the lock-down for instance. The most shocking though, is that 26% do not plan for significant change in its life due to Covid19. It is not clear for me whether it is an indication of tremendous confidence or ignorance.

Digital adoption

Forced by the lock-down, digitization has increased significantly in previously intact consumer segments. Similar to global phenomenon, a weekly one day home office typical of some sectors before Covid19 became standard, where it was applicable. Food delivery and online retail trade, mainly grocery have grown exponentially. All of the other goods and services showed a similar increase that could be purchased online before the pandemic or if their sales model could be switched to online quickly. Due to the closure of physical customer services during lock-down, the online payment of utilities has exploded, most of the consumers did it digitally for the first time in their lives, while the increase of other activities done online was similar. Cashless payment increased substantially. According to the survey, the ‘digital comfort’ of clients increased by 50%, of which 26% felt the improvement significant. In my view, however, it cannot be stated that the solutions are state-of-the-art in customer experience and powered by most recent technology. Instead, the clients were capable to make simple actions in a forced situation.

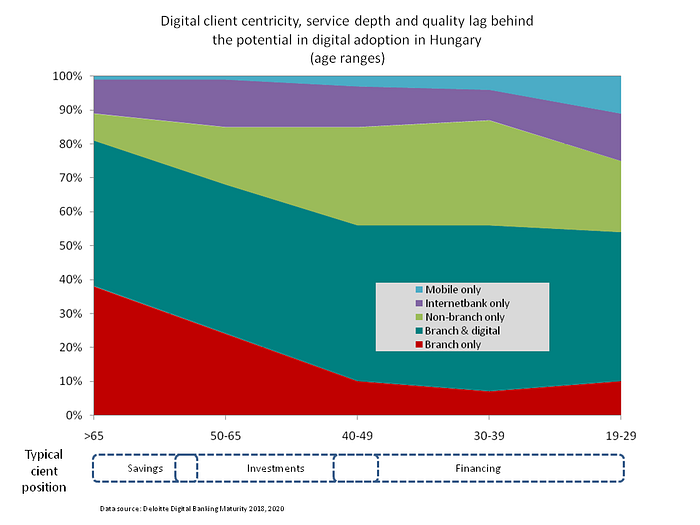

36% of Hungarian banking customers have been forced to digitally adapt meaning that the number of branch-only customers has decreased by that figure. Beyond branches, they started to use call-center, internet banking, and mobile banking. More remarkable that 16% have switched to digital-only channels. The modest growth of mobile-only clients is somewhat surprising. One possible reason for that is the services available on this platform are simply not there yet to be full-fledged alternatives to more mature channels. The question and the challenge are how durable is this jump in non-branch on the client’s side. Are they able to go through entire processes in a simple, client-friendly way digitally even including personal or at least personalized advice in relevant client journeys and segments? If not, they will go back to the branches as soon as they can. To make the picture more shadowed, rental fees eye-witnessed a 20–30% decline, maybe not reaching the bottom yet, which can induce renegotiations or relocations to improve branch profitability.

What is durable out of Covid19 impacts in Call-center, Internet bank, and Mobile bank?

What is striking is that in the under 50 years age range approx. 50% are already digital-only customers, while under 30 years there is more internet bank only and dynamically growing mobile bank only customers together than call-center users. These clients less and less turn to the call-center for banking. In the last more than a decade, the drivers for the developments of digital channels were product-based: gradual extension from basic services, accounts, payments, bank cards then securities, etc. Out of the current situation, the changing role of the call-center and more targeted customer experience-based mobile and internet banking developments would follow based on forward-looking customer value modeled customer segmentation. While the branch channel remains for personal advice, for regular portfolio reviews, for specific client needs, or in case of financial net worth above a limit, but not for a transaction.

One of the interesting questions within a year horizon is who will implement and what developments in digital channels induced by the challenges and impacts of Covid19, specifically? How fast the digital developments could be? Cooling the expectation let me cite the example of Google. It required the explosion of Zoom and took nearly two months (March 9: Italian quarantine, April 29: announcement) to make its 2017 product Meet available to everyone for free amidst a global crisis.

In addition to the spread of digital, what can be expected in some other banking relevant areas? Similar to recent years, growth in precautionary savings will likely be channeled to finance state budget and debt due to the crowding-out effect of those securities. This likely will be the major trend despite some increase in crisis resistant investments and the fact that many see stock markets as points of entry due to perceived undervaluation and will take positions. The controlled weak HUF is in the interest of the economic policy. A significant proportion of customers have applied for the lending moratorium. Transaction turnover plummeted. Fear of the risks of the second Covid19 wave will intensify. Accumulated, unsold stocks of goods led to a temporary drop in prices via imports as a very short-term effect even despite stronger depreciation of HUF. Already in the short-term though, in addition to cost reduction, I expect price increases in general with the exceptions of segments hardly hit, such as real-estate. The dynamically increasing spending on foreign holidays in recent years will not be switched automatically as a whole to domestic tourism, which is over-valued on the price per value basis for the local middle class. The pressure is strong to increase budget revenues with the main reasons the economic slow-down, the skyrocketing costs of the Covid19 defense, and the specific structure of state economic boost measures. Therefore, the government continues to whiten the economy, it will boost non-productive public sector investments and increase revenues through municipalities. All these likely results in higher expenditure for the clients. The corporate segment is exposed to global, mainly WEU economic climate with the exception of construction.

What does this mean for the banking sector?

Re-planning 2020–2021, with adjusting sales and investment plans, extra work in reviewing and monitoring credit risk, restructuring efforts, increase in provisions, and write-offs. Cost reduction is inevitable according to the classic recipe: cut in external services, marketing, then canceling wage increase, bonuses, to close with flat layoffs without major structural changes. Despite state product schemes, client focus becomes short-term in increased uncertainty, thus retail credit demand is slower than planned. There is a long list to adjust and a higher uncertainty in income. However, many lessons have been learned in the last global crisis and banks are better prepared in terms of financial health, systems, procedures, crisis, and management.

The longer-term is markedly influenced by several factors.

When there will be a widely available effective vaccine, treatment to eradicate the epidemic, the mutations in the virus, and how this will change the perception of uncertainty for customers, regulators, bank owners, and the market in general. This is new.

The rest is with us in the last 10 years or so. These are the longer-term measures at the international, governmental, and parent institutions or owners level.

In Hungary, banking strategies have been for many years predominantly influenced by:

- the international and domestic regulatory environment strengthened heavily following the last global financial crisis

- the economic policy through financial programs (NHP, CSOK etc.), or

- structurally (compulsory private pension funds, house savings co-operatives, instant payment)

- the changes in the ownership of local banks, merger

- the financial health and strategies of foreign parent banks

- and, to a surprisingly lesser extent, the organic customer needs.

Whether the UX centric digital transformation will fall victim to inevitable short-term adjustments or, as the opposite, it will be accelerated, is yet to be seen.

If you like this article, follow me and read other stories.

Visit www.istvansebestyen.com for more.